Before diving into how a mortgage works, let’s understand what a mortgage is.

What is a mortgage?

A mortgage is a loan that a borrower uses to maintain or purchase a home and other forms of real estate that they agree to pay back over time. In a mortgage, the property serves as collateral to secure the loan. Simply, a mortgage is a loan you get from a lender to finance a home purchase. Through a series of repayments, the borrower then pays back the loan with interest. Here the lender is listed on the title of the property until the borrower fully repays the entire loan.

What are the types of mortgages a borrower can choose?

Borrowers can choose from a fixed-rate mortgage or a variable-rate mortgage.

Fixed-rate mortgage

As the name suggests, a fixed-rate mortgage is a type of mortgage where the interest rate is locked for a certain time, usually between one to five years. So, whether the lender’s rate goes up or down, you will be making the same home loan repayments.

Advantage of fixed-rate mortgage:

- An ideal choice for people who want to budget with certainty for e.g. first time home buyers and investors who want to ensure a consistent positive cash flow

- A fixed-rate mortgage prevents sudden hikes in interest rates especially when it is unexpected

Disadvantage of fixed-rate mortgage:

- Borrowers will not be able to benefit when the interest rates go down.

- Making extra repayments incur additional fees above a threshold limit.

- Borrowers may not have access to redraw accounts.

- Clients have to pay break costs if they wish to change the product from fixed to variable before the expiry of the fixed-rate term.

What are the types of mortgages a borrower can choose?

Borrowers can choose from a fixed-rate mortgage or a variable-rate mortgage.

Fixed-rate mortgage

As the name suggests fixed-rate mortgage is a type of mortgage where the interest rate is locked for a certain time. Usually between 1 to 5 years. So, whether the lender’s rate goes up or down, you will be making the same home loan repayments.

Advantage of Fixed-rate mortgage:

- An ideal choice for people who want to budget with certainty for e.g. first time home buyers and investors who want to ensure a consistent positive cash flow

- A fixed-rate mortgage prevents sudden hikes in interest rates especially when it is unexpected

Disadvantage of fixed-rate mortgage:

- Borrowers will not be able to benefit when the interest rates go down.

- Making extra repayments incur additional fees above a threshold limit.

- Borrowers may not have access to redraw accounts.

- Clients have to pay break costs if they wish to change the product from fixed to variable before the expiry of the fixed-rate term.

Variable-rate

The interest rate can change over time in the case of a variable-rate mortgage. Whenever the interest rate goes up, the repayments increase. However, you do have the benefit of saving if the interest rate decreases. Some people choose variable rates because it offers a lot of flexibility compared to fixed-rate mortgages.

Advantage of variable-rate mortgage:

- Provides more flexibility than fixed-rate mortgages

- Ideal for homebuyers with fluctuating income

- Ideal for people who would like to keep their savings in an offset account and benefit from reduced interest repayments

Disadvantages of variable-rate mortgage:

- Unlike a fixed-rate mortgage, the variable rate mortgage is exposed to varying interest rates and is dependent on the current market

- Your monthly payments increase significantly if the interest rate increases

Studies show that borrowers are likely to pay less interest overall with variable-rate loans versus fixed rates. However, historical trends are not necessarily indicative of future performance.

Parties involved in Mortgage

There are two parties involved in the mortgage – a lender and a borrower.

Lender

A lender is a financial institution that offers you loans to buy a home. Your lender might be a bank or it can also be an online mortgage company. The lender will review your information to make sure that you meet their standards. Every lender has its terms and standards for loaning money. The lender goes through your full financial profile including credit score, income, debts, your assets. The information helps them to assess whether you will be able to make your loan payment on time.

Borrower

A borrower is an individual seeking a loan. You may be able to apply for a mortgage loan as the only borrower or with a co-borrower. You can be qualified for a more expensive home by adding more borrowers with income for your loan.

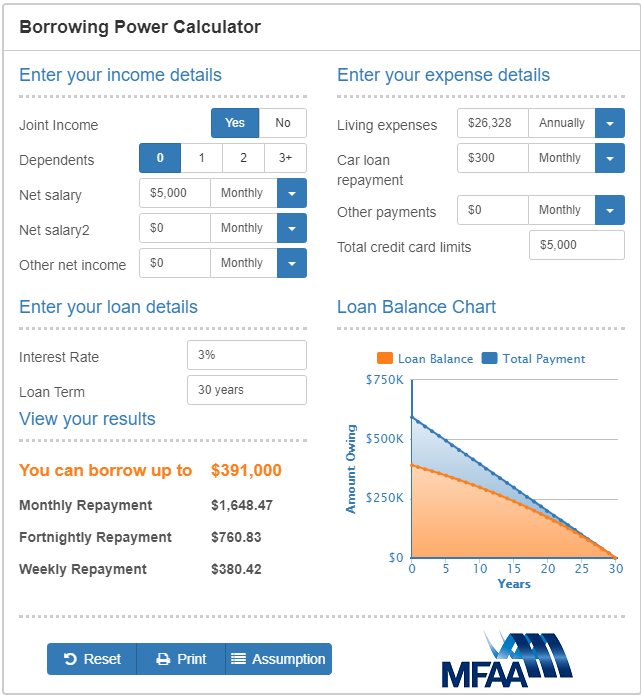

How much mortgage can you afford?

Most people want to know how much they can afford to spend before they apply for a mortgage. Well, this depends on the type of loan and the interest rate you choose. You can use our How much can I borrow calculator which can give you a good indication of your borrowing capacity.

How long does it take to pay off your mortgage?

One of the common questions asked in the mortgage process is how long it will take to pay a mortgage. Most lenders offer loans for up to 30 years, but there are ways so that you can pay it sooner. Some of the features that can help you to pay off your mortgage sooner are:

- Additional Repayment

- Redraw

- Offset Account

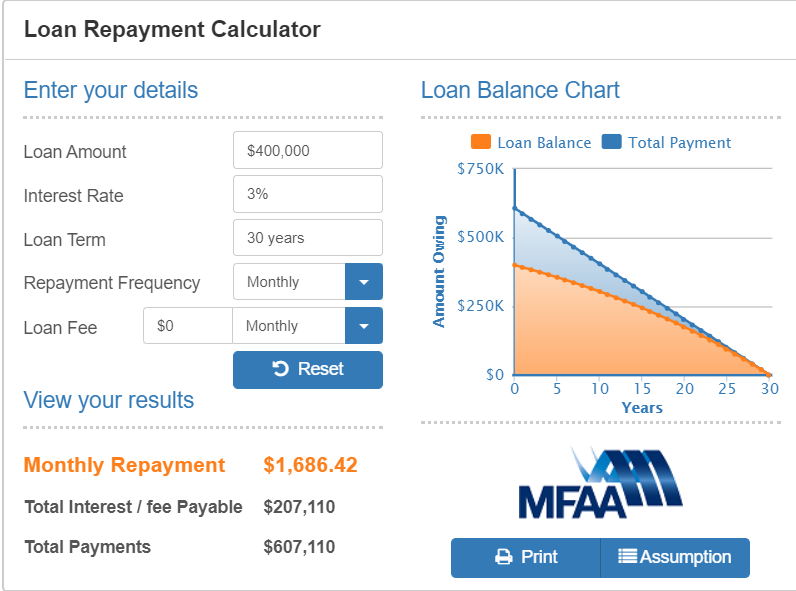

How much are mortgage repayments?

Most of the borrowers want to know how much their mortgage repayments will be. You can use our loan repayments calculator to get a rough idea about it.

Knowing the basics of mortgages can help you understand exactly what you are looking for. There are different types of interest rates. To understand how much you can afford and what it takes to be eligible for a mortgage loan, use our free assessment.